Investment Solutions for Inflation-Protected Income

By Gene Balas, CFA®

Investment Strategist

Executive Summary

With high inflation affecting everyone’s day to day lives, many investors are concerned with protecting their income from inflation. Two potential solutions to help with this problem are Series I Savings Bonds and TIPs. There are many nuances to note with each of these vehicles before making an informed decision.

For investors looking for ways to earn an inflation-adjusted return, there are a number of solutions we’ve touched on in previous communications.

One strategy that’s recently been gaining in popularity is I-Bonds. These are U.S. savings bonds whose interest payments include a variable rate that changes with inflation combined with a fixed rate (which is currently zero). The other more widely used solution is Treasury Inflation Protected Securities (TIPS)—U.S Treasury notes whose principal adjusts annually based on the previous year’s inflation rate. Both options have slightly different pros and cons, as well as nuances.

A Closer Look at I-Bonds

I-Bonds were created more than two decades ago to help Americans protect their savings from rising prices. U.S. government Series I-Savings Bonds pay a fixed interest rate (set at the time of purchase) along with a variable interest rate which regularly adjusts to reflect the past six months’ level of inflation as measured by the Consumer Price Index. Interest accrues monthly—for up to 30 years if the bond is held to maturity.

However, there’s a limit to the quantity of I-Bonds investors can purchase:

- Online, you can buy up to $10,000 worth of bonds each calendar year (per Social Security number).

- Additionally, you can buy up to $5,000 of paper bonds annually using your income tax refund.

- The individual limit, therefore, is $15,000 per calendar year per Social Security number. (Note: you may purchase additional bonds for each household member with a unique Social Security number)

And all I-Bonds must be purchased through the treasurydirect.gov website; they cannot be bought through a brokerage firm.

With surging inflation over the past year, I-Bonds purchased before November 1st, 2022 will pay 4.81% interest for the first six months (or 9.62% on an annualized basis), then a new rate will be determined in November according to September’s CPI inflation reading. Rates are adjusted every May and November, but the initial interest rate you receive covers the first six months following the date of purchase. Therefore, any bonds purchased through the end of October will have the rate noted above applicable for the subsequent six months.

Of course, if inflation decreases—which is currently the Federal Reserve’s primary goal—the adjustable rate attributed to inflation will also be lower. Let’s say prices rise 3% from April through September. You would receive a 4.81% yield the first six months, and 3% for the next 6 months (or a yearly 7.85% rate when compounding after the first six months). Note that the fixed rate component (currently 0%) generally coincides with the short-term interest rates set by the Fed. The history of both the fixed and the variable rates are available here:

I-Bonds also carry some important caveats:

- They cannot be sold for at least one year from the date of purchase.

- If redeemed before five years, you are required to forfeit three months of interest.

- They don’t make regular interest payments in cash. Instead, interest is added on to the principal value of the bond, and the higher value will then accrue interest, compounded, until the I-Bond is ultimately sold or matures (where it pays the accrued interest and principal).

- Their interest income isn’t subject to state or local taxes (though it is subject to federal taxes).

Given that I-Bonds don’t pay interest income in cash, they may not be an optimal solution for generating supplemental income or cash flow. On the plus side, taxes won’t be due until you actually receive the interest (you do have the option to pay income taxes annually as income accrues). However, because I-Bonds already come with this element of tax deferral, they can’t be held inside an IRA.

For parents and grandparents, I-Bonds may be another tax-efficient way to save for a child’s education, as you can potentially avoid paying federal taxes if the I-Bonds are used for education expenses, subject to the conditions stated here.

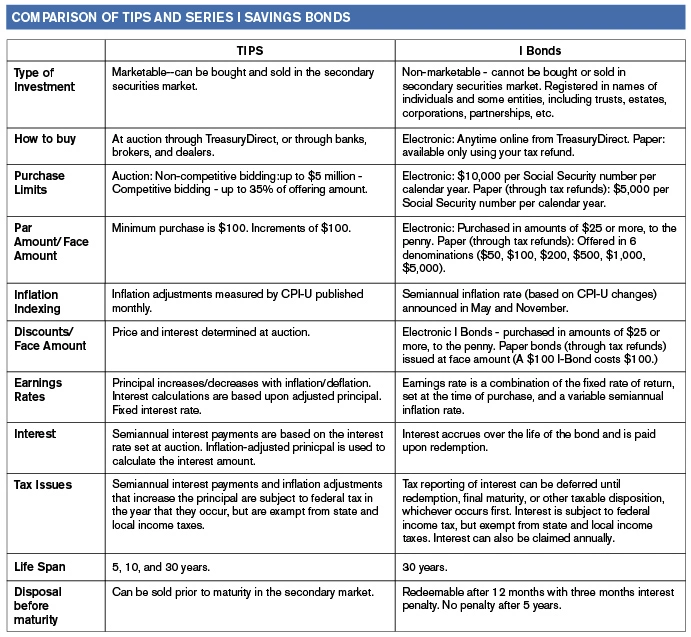

Comparing I-Bonds with TIPS

Like I-Bonds, TIPS include an element of inflation protection. An important distinction, however, is that the principal values of TIPS are adjusted to incorporate ‘the ex-post inflation rate in an annual adjustment,’ whereas I-Bonds receive an adjustment in their interest rates to reflect inflation. This means the interest rate on a TIPS bond is determined at the time of issuance, but as with any bond, its yield is a function of both the coupon interest rate and the price at which you purchase it. (And since a TIPS bond will see its principal value increase with the inflation adjustment, your interest income likely increases as well.)

Moreover, TIPS sell on the secondary market, and are available in mutual funds and ETFs. This gives TIPS investors an element of liquidity that’s not available for I-Bond investors, who need to wait at least 12 months after purchase to redeem their bonds.

TIPS also provide you with regular, semiannual interest payments; whereas I-Bond investors only receive their accrued income when they sell. This generally makes TIPS preferable to I-Bonds if you’re seeking current income.

Unlike I-Bonds, however, the tax treatment of TIPS is not deferred until maturity or sale. TIPS investors must pay tax on their income payments, as well as the inflation adjustment made to their principal values—unless of course they are purchased and held in a tax-advantaged account such as an IRA.

Keep in mind, though, that the price of TIPS can fluctuate to the downside. As with most bonds, any increase in prevailing interest rates will tend to negatively impact TIPS prices; although the market’s assessment of inflation will complicate the value calculation. And TIPS’ yields are usually lower than that of conventional Treasury bonds of the same maturity—unless the market expects deflation to occur.

The difference between the yield of a TIPS bond and a Treasury bond of the same maturity reflects the market’s expectations for inflation over the life of the TIPS bond. If inflation exceeds expectations, you will come out ahead by investing in a TIPS bond rather than a conventional Treasury bond. If inflation falls short of those market-based expectations, you would have been better off investing in a conventional Treasury bond. In finance terms, these inflation expectations are known as ‘breakeven rates.’ They can fluctuate quite a bit over time, as seen in the adjacent graph showing the generic five-year TIPS bond as of July 8, 2022:

Source: Bloomberg

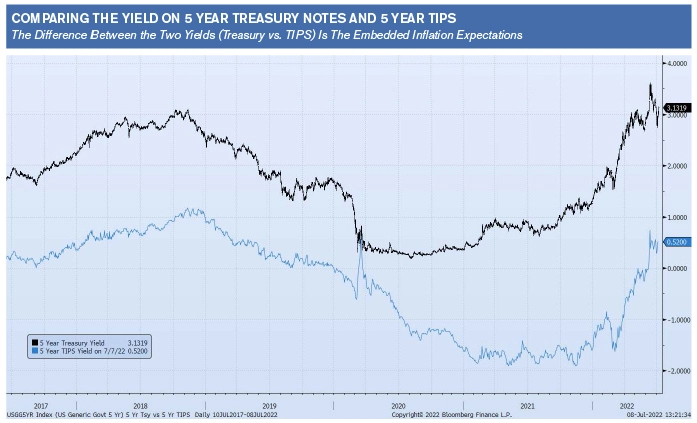

In this case, the embedded expected inflation rate over the next five years is about 2.6%. If actual inflation exceeds that rate, it will produce a higher return. This is because the yield on a TIPS bond is much less than the comparable yield on a nominal Treasury bond. In fact, some TIPS have even delivered negative yields in recent years—as depicted in the adjacent graph comparing five-year TIPS yields to the yields of conventional Treasury bonds:

Source: Bloomberg

Why negative? Because inflation expectations rose much faster than the yields on conventional Treasuries. Investors were willing to accept a negative yield by paying a higher price for a TIPS bond that would later mature at a lower par value (excluding inflation adjustments) because they were confident that inflation adjustments would more than compensate them for the difference in yields. By contrast, I-Bonds don’t change in price, and it is only their yield—not their price—that reflects the inflation compensation.

Summary

I-Bonds and TIPS are just two of the many different asset classes that can help you adjust your portfolio to address high or rising inflation. Both can be employed to obtain a potentially favorable return when factoring in inflation. And you don’t have to make an ‘either/or’ decision. You can rely on a mix of both—in tandem with other suitable assets—as an effective inflation hedge. Talk to your advisor; he or she will help you decide on an optimal mix of assets to meet your needs, along with a strategy for how best to implement that decision

The information contained herein is for informational purposes only and should not be considered investment advice or a recommendation to buy, hold, or sell any types of securities. Financial markets are volatile and all types of investment vehicles, including “low-risk” strategies, involve investment risk, including the potential loss of principal. Past performance does not guarantee future results. For details on the professional designations displayed herein, including descriptions, minimum requirements, and ongoing education requirements, please visit seia.com/disclosures. Signature Estate & Investment Advisors, LLC (SEIA) is an SEC-registered investment adviser; however, such registration does not imply a certain level of skill or training and no inference to the contrary should be made. Securities offered through Royal Alliance Associates, Inc. member FINRA/SIPC. Investment advisory services offered through SEIA, 2121 Avenue of the Stars, Suite 1600, Los Angeles, CA 90067, (310) 712-2323. Royal Alliance Associates, Inc. is separately owned and other entities and/or marketing names, products, or services referenced here are independent of Royal Alliance Associates, Inc.

Third Party Site

The information being provided is strictly as a courtesy. When you link to any of the websites provided here, you are leaving this website. We make no representation as to the completeness or accuracy of information provided at these websites. Nor is the company liable for any direct or indirect technical or system issues or any consequences arising out of your access to or your use of third-party technologies, websites, information and programs made available through this website. When you access one of these websites, you are leaving our web site and assume total responsibility and risk for your use of the websites you are linking to.

Dated Material

Dated material presented here is available for historical and archival purposes only and does not represent the current market environment. Dated material should not be used to make investment decisions or be construed directly or indirectly, as an offer to buy or sell any securities mentioned. Past performance cannot guarantee future results.