Runaway Inflation or Reflation?

By Josh Woodard, CFA®

Research Analyst

Summary

- With unemployment levels still elevated, inflation should not be a short term concern

- The Fed has made clear their intention to maintain rates at low levels for the foreseeable future—even if inflation meets or surpasses their historical 2% target

- Asset classes such as real assets, commodities, equities, and TIPS provide a good hedge against inflation

Where do we stand today?

Not too long ago, the economy was coming to a screeching halt and deflation concerns were top of mind. Deflation is typically a feared situation—indicating that an economy has stalled and yet consumers continue to defer spending despite falling prices. Modest inflation, on the other hand, is generally a positive sign, as it points to a healthy, growing economy.

What we know today is that market expectations for inflation have certainly rebounded as indicated by the 10-year Breakeven Inflation Rate, which has bounced back to 1.77% as of 9/11/2020.

At Jackson Hole, WY on August 27, Federal Reserve Chair Jerome Powell formally announced a new policy path that should have significant market implications going forward. According to Powell, the Fed intends to keep interest rates low and let inflation run for longer than usual. Remember, the Fed has two primary monetary policy goals: maximum employment and stable inflation (measured by Personal Consumption Expenditures). Historically, the Fed has aimed for a 2% inflation target—meaning that while short-term dips and spikes may occur, inflation should consistently run at about 2%.

While this new policy is subject to interpretation, the main takeaway is that the Fed will not raise rates when and if we see inflation tick across the 2% threshold. Bottom line: The Fed is hoping to spur economic growth, and in turn, see that growth trickle down to wage growth and a healthy rise in prices.

What will drive inflation?

Currently, runaway inflation is not a concern for SEIA’s Investment Committee. While the July and August prints showing some bounce-back in inflation are encouraging, we see no current signs of high inflation. Of course, this could change. But first, there are some structural issues that will need to be worked out.

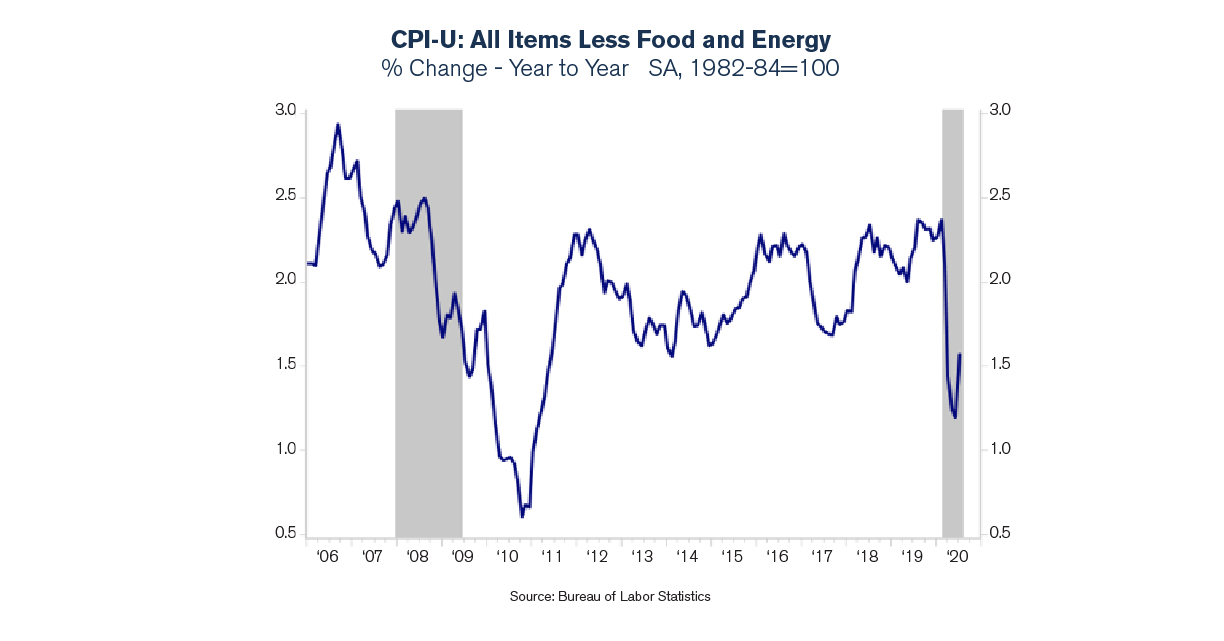

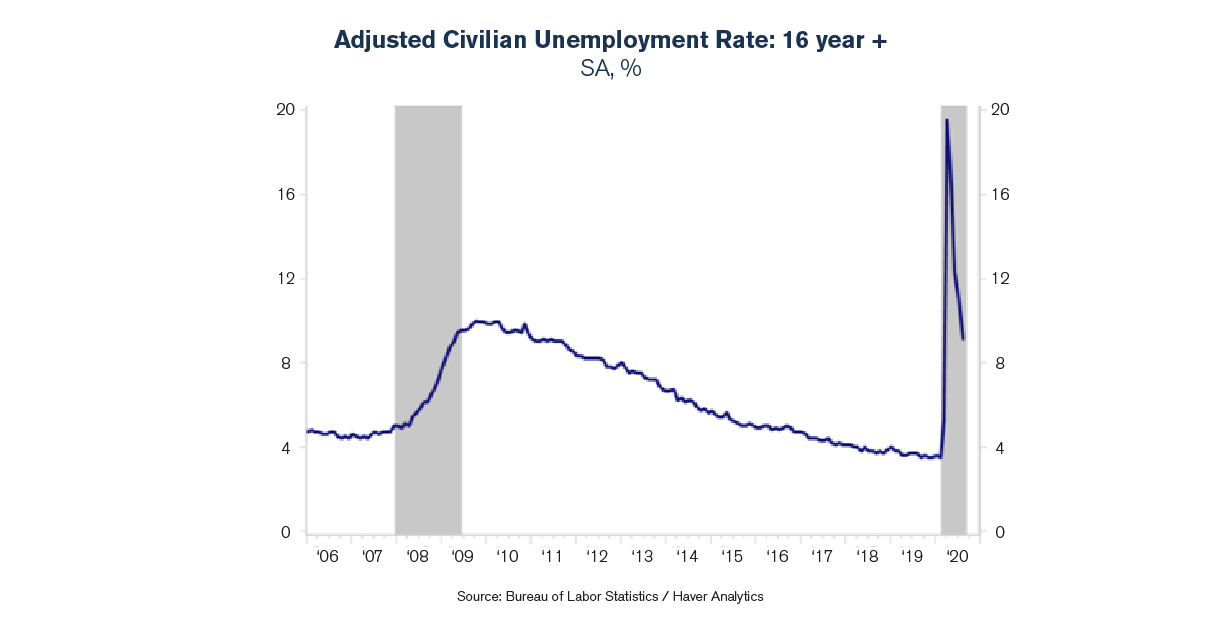

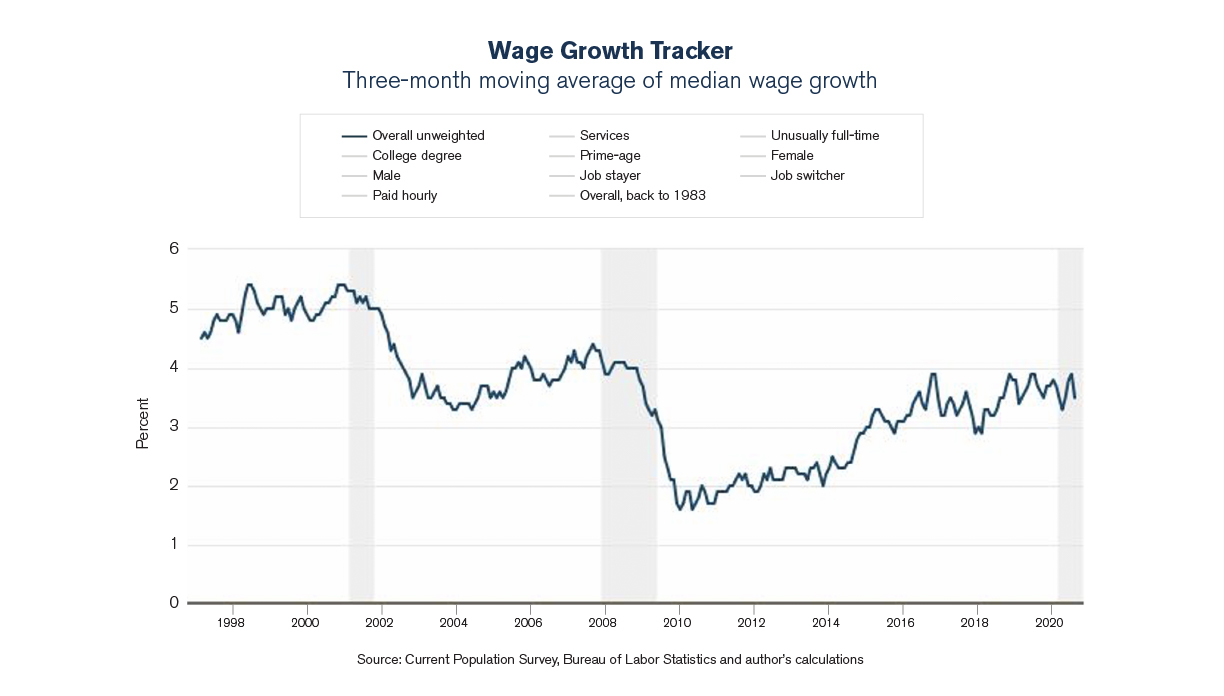

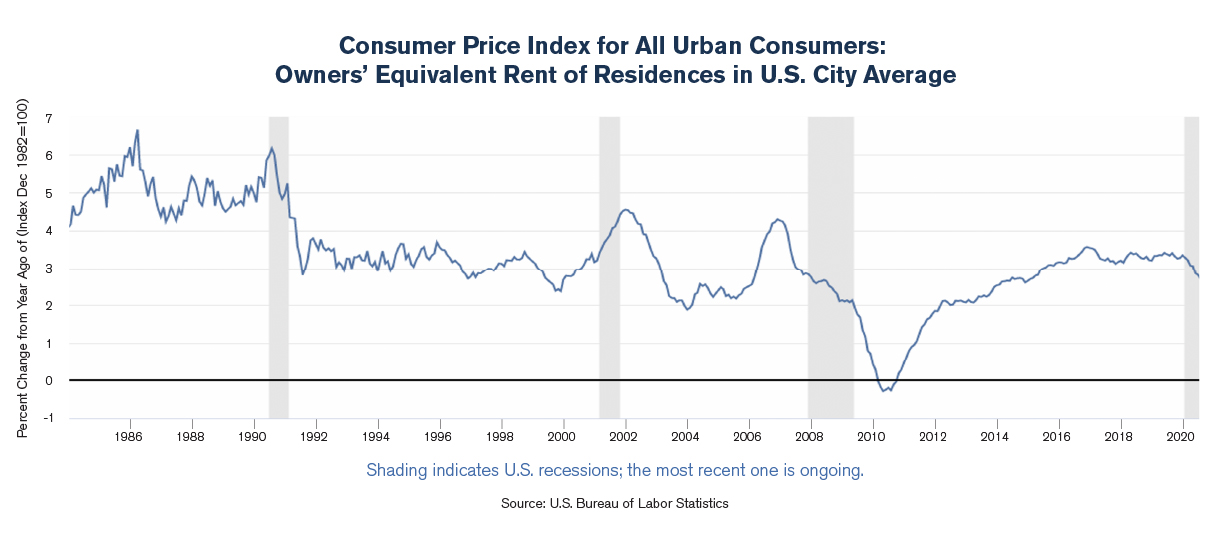

Inflation is measured as a basket of goods and services. So, to see a significant rise in inflation, almost the entire basket would need to go up. Since housing/shelter costs account for one-third of the Consumer Price Index (CPI) basket, we closely monitor residential rents along with wages, for signs of sustained inflation. With unemployment at present high levels (8.4%), however, we expect that it will take a fair amount of time for wages and rents to pick up meaningfully.

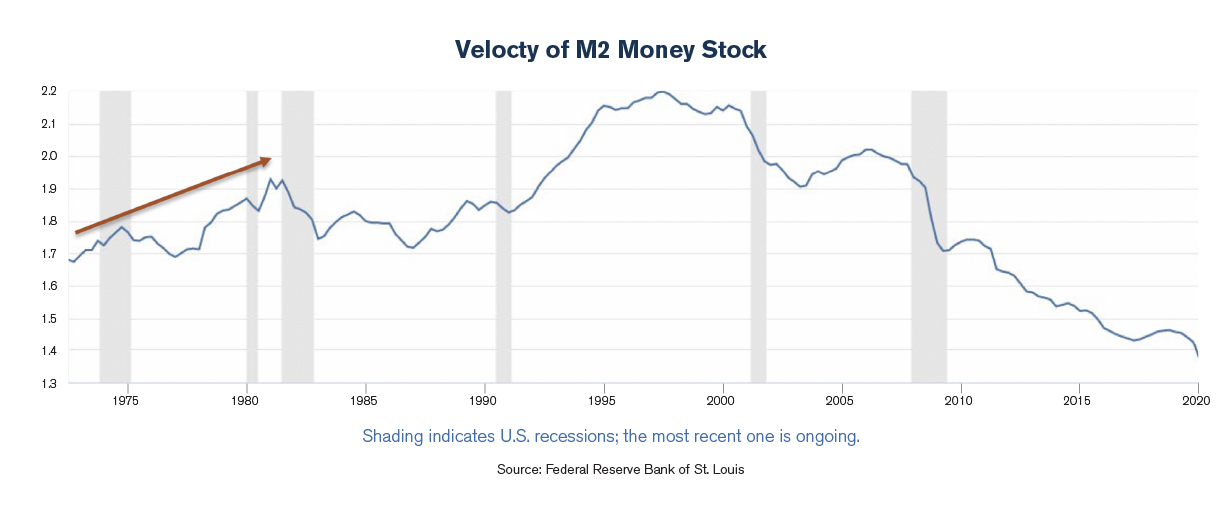

While current monetary policy has steadily fueled the money supply, the increase in supply alone should not cause inflation. Instead, it’s the velocity of that money which potentially leads to inflation. The velocity of money can be defined as the rate of money being exchanged between individuals in an economy. As more transactions take place (e.g., You go out and buy a car, the car salesman in turn goes out and buys a house, which allows the mortgage broker to take a vacation, etc.) this number increases.

There are other factors that could lead to inflation, such as a supply shock to certain industries. This was precisely the driver of the high inflation experienced during the 1970s—as the 1973 oil shock sent energy prices soaring. Additionally, a pickup in fiscal policy could potentially lead to a pickup of inflation (e.g., a massive infrastructure package). The 20’s could very well wind up being the decade of joint monetary and fiscal spending, but we’re not there yet (perhaps after the election).

What assets can help hedge against inflation?

Asset classes that have historically provided solid inflation protection include real assets, commodities, equities, and Treasury Inflation Protected Securities (TIPS).

Real assets are physical assets well suited for hedging inflation—things like real estate and infrastructure which are attractive due to their cash flow. For example, when housing costs begin to rise, landlords are able to raise their rents to offset the impact of inflation. Compared to owning an asset like a fixed rate bond, this feature makes real assets highly attractive during inflationary times.

Gold, silver, and other precious metals typically hold up well to inflation as a result of a weakening U.S. Dollar in this type of environment. And commodities such as oil and energy products are also good inflation hedges as their costs tend to rise with inflation.

TIPS are specifically designed to help protect against inflation-induced fixed rate bond losses. The price of TIPS will increase as current inflation and future expectations increase. Semi-annually, TIPS interest payments will also adjust.

Finally, stocks tied to the economy can serve as solid inflation hedges thanks to the pricing power many companies have—allowing them to keep pace with inflation. During periods where both the economy and inflation are growing, stocks have historically outperformed inflation. In fact, small cap equities have outperformed inflation every decade going back to the 1930s.

Conclusion

While current data shows significantly higher inflation expectations compared to the lows we experienced back in Q2, it does not appear to pose any serious risk. The adoption of this new Fed policy may lead to systemic inflation somewhere down the road, depending on how far beyond the 2% target they’ll allow inflation to run before starting to raise rates. Money printing alone, however, won’t be the culprit. We will also need to see a meaningful pickup in the circulation of this money through the economy. In the meantime, hard assets and assets with regular cash flows can offer investors solid protection against future inflation.

Although the information has been gathered from sources believed to be reliable, it cannot be guaranteed. View expressed in this newsletter may not reflect the views of Royal Alliance Associates Inc. Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss. Past performance is no guarantee of future results. Please note that individual situations can vary. Therefore, the information presented here should only be relied upon when coordinated with individual professional advice.

Signature Estate & Investment Advisors, LLC (SEIA) is an SEC-registered investment adviser; however, such registration does not imply a certain level of skill or training and no inference to the contrary should be made. Securities offered through Royal Alliance Associates, Inc. member FINRA/SIPC. Investment advisory services offered through SEIA, 2121 Avenue of the Stars, Suite 1600, Los Angeles, CA 90067, (310) 712-2323. Royal Alliance Associates, Inc. is separately owned and other entities and/or marketing names, products, or services referenced here are independent of Royal Alliance Associates, Inc.

Third Party Site

The information being provided is strictly as a courtesy. When you link to any of the websites provided here, you are leaving this website. We make no representation as to the completeness or accuracy of information provided at these websites. Nor is the company liable for any direct or indirect technical or system issues or any consequences arising out of your access to or your use of third-party technologies, websites, information and programs made available through this website. When you access one of these websites, you are leaving our web site and assume total responsibility and risk for your use of the websites you are linking to.

Dated Material

Dated material presented here is available for historical and archival purposes only and does not represent the current market environment. Dated material should not be used to make investment decisions or be construed directly or indirectly, as an offer to buy or sell any securities mentioned. Past performance cannot guarantee future results.