Oil, oil everywhere…

By Sam Miller, CFA®, CFP®, CAIA®

Senior Investment Strategist

What happened?

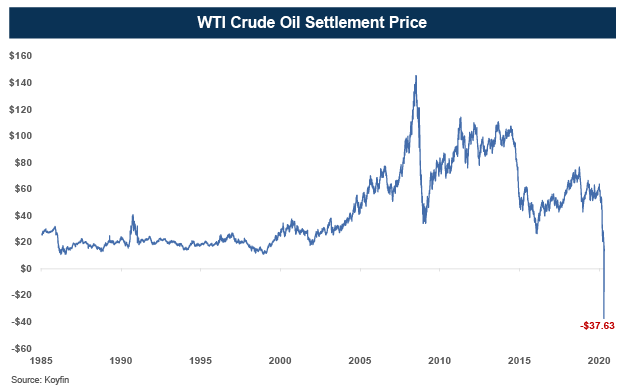

In a year already filled with memorable days, Monday, April 20th will be remembered as a historic one for the markets – with the price of West Texas Intermediate crude oil dropping below zero for the first time ever (closing at -$37.63/bbl). While this slide is the result of the world’s supply of oil vastly exceeding demand at a time when governments try to limit the spread of COVID-19, the negative price action was a byproduct of the “quirks” associated with how oil is traded and priced (i.e., futures contracts require buyers to take possession of oil). Ultimately, it serves as yet another consequence of the unprecedented, immediate shutdown of the global economy and is just the latest record to be set in an already historic 2020.

How is this possible?

The devastating economic impact of COVID-19 business closures and stay-at-home orders has sharply reduced demand for oil. At the same time, producers can’t cap their oil wells fast enough to reduce supply to match this lower demand. Steps to restrain production and support prices have had limited success thus far. Exacerbating the problem is the fact that oil storage facilities are nearing full capacity. The result is that producers are having to pay to get rid of their oil (negative prices).

While there’s much more involved in how prices went negative – including the math for how financial derivatives are computed, and how tankers, oil pipelines, refineries, and oil wells are managed – the overarching concern is that the energy markets are experiencing unprecedented turmoil. Producers have been cutting production, but according to the U.S. Energy Information Administration (EIA), if the pace of inventory increase continues U.S. storage tanks will be completely full in less than two months. Even with Saudi Arabia striking a deal to cut production by 10 million barrels per day, much more will need to happen before the global oil market can find its balance.

What do low oil prices mean for oil companies?

As you might imagine, low (and negative) oil prices are a big problem for the profitability of oil producers. They have to cut back on production to match demand, while at the same time financing costs for the sector have risen. The risk of smaller producers going out of business has escalated dramatically, and it’s likely the industry will look much different when our economy eventually comes back online. Around 80 oil and gas companies filed for bankruptcy in the 2015 sell-off; this current situation is far worse. In fact, a recent Kansas City Federal Reserve Bank survey indicates that nearly 40% of oil companies say they will be insolvent within a year if oil prices remain at or below $30/barrel1.

What does this mean for consumers and investors?

Under normal circumstances, lower oil prices help consumers by pushing down inflation and boosting spend power. At the moment, however, that’s not happening since people aren’t driving and most retailers are shuttered. Once the economy comes back online, demand will increase and prices should rise accordingly.

In the near term, investors should expect more volatility for energy markets and energy stocks until the supply and demand imbalance can be corrected. Since it takes a considerable amount of time for oil producers to shut down facilities, don’t expect the oil market to calm down anytime soon.

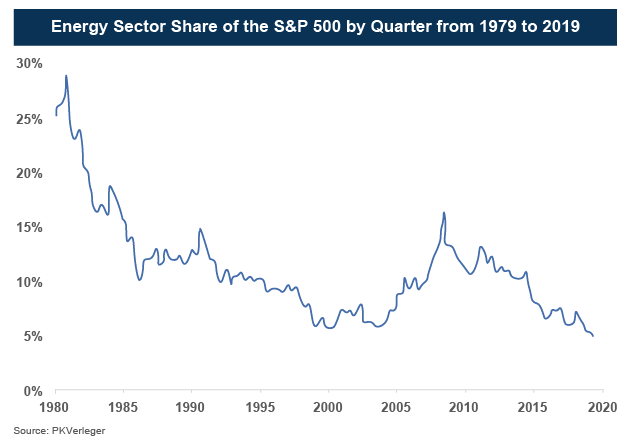

While the negative oil price headlines are sensational, and we’re unquestionably living in unprecedented times, it’s important to keep the historic importance of the energy sector in mind. Back in 1980, the sector made up nearly 30% of the S&P 500®. Today it makes up less than 3%.

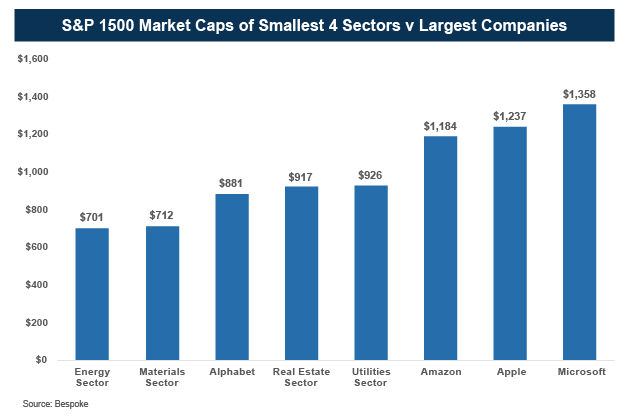

To offer an additional perspective, the combined market value of every energy and materials company in the S&P 500 today is barely bigger than Microsoft. Each of the big four internet stocks by themselves are currently bigger than the entire S&P 500 energy sector.

To offer an additional perspective, the combined market value of every energy and materials company in the S&P 500 today is barely bigger than Microsoft. Each of the big four internet stocks by themselves are currently bigger than the entire S&P 500 energy sector.

Despite the energy sector’s relative importance eroding in recent decades, the S&P 500 as a whole has still managed to provide an average annual return of about 11% since 1980, a strong reminder of the benefits of diversification2. Both oil and stock prices are sure to remain volatile, especially in the short-run, but any further bad news for the energy industry should only have a modest impact on the broader stock market and diversified portfolios.

Despite the energy sector’s relative importance eroding in recent decades, the S&P 500 as a whole has still managed to provide an average annual return of about 11% since 1980, a strong reminder of the benefits of diversification2. Both oil and stock prices are sure to remain volatile, especially in the short-run, but any further bad news for the energy industry should only have a modest impact on the broader stock market and diversified portfolios.

We believe investors with a long-term perspective will continue to be rewarded over the long-term. Lastly, we appreciate the trust and confidence you place in us, especially during these historic times. Don’t hesitate to reach out to your advisor if we can be of service.

1 Federal Reserve Bank of Kansas City, First Quarter Energy Survey, “Tenth District Energy Activity Decreased as a Steep Pace,” April 7, 2020.

2 Bloomberg

Securities offered through Royal Alliance Associates, Inc. member FINRA/SIPC. Investment advisory services offered through SEIA, LLC, 2121 Avenue of the Stars, Suite 1600, Los Angeles, CA 90067, (310) 712-2323. Royal Alliance Associates, Inc. is separately owned and other entities and/or marketing names, products or services referenced here are independent of Royal Alliance Associates, Inc.

Third Party Site

The information being provided is strictly as a courtesy. When you link to any of the websites provided here, you are leaving this website. We make no representation as to the completeness or accuracy of information provided at these websites. Nor is the company liable for any direct or indirect technical or system issues or any consequences arising out of your access to or your use of third-party technologies, websites, information and programs made available through this website. When you access one of these websites, you are leaving our web site and assume total responsibility and risk for your use of the websites you are linking to.

Dated Material

Dated material presented here is available for historical and archival purposes only and does not represent the current market environment. Dated material should not be used to make investment decisions or be construed directly or indirectly, as an offer to buy or sell any securities mentioned. Past performance cannot guarantee future results.